Why is it better to regularly Pre-pay part of your Home Loan? | A Comprehensive Guide

Owning a home is a dream for every family, but owning it often involves taking out a loan. A loan is a long-term financial commitment, and finding ways to optimize it can lead to substantial savings and financial security. One practical and effective strategy homeowner can employ is regularly pre-paying a portion of their home …

Owning a home is a dream for every family, but owning it often involves taking out a loan. A loan is a long-term financial commitment, and finding ways to optimize it can lead to substantial savings and financial security. One practical and effective strategy homeowner can employ is regularly pre-paying a portion of their home loan. In this article, I will explain why it is better to pre-pay part of your home loan prepayments regularly and ways to do it.

Understanding Home Loans and Prepayment

Before we get into the benefits of pre-paying a home loan, it’s essential to understand what home loans and prepayments are;

What is a Home Loan?

A home loan is a financial product that allows individuals to purchase a home by borrowing money from a lender (bank). The borrower (you) agrees to repay the loan amount over a specified period, usually 15, 20, or 30 years, along with interest.

What is Prepayment?

>Home loan prepayment refers to making additional payments toward the principal loan amount in addition to the regular EMI (Equated Monthly Instalment). These extra payments can be made anytime, reducing the loan’s outstanding balance. However, rules differ from bank to bank. Many banks do not allow the borrower to make early prepayments as the bank knows the maximum interest they can earn as a lender is at the beginning of the loan tenure. Hence, checking prepayment conditions while you opt for the loan is essential.

Related Article : Latest Floating Rate Reset Rules on Loans | RBI’s (2023) Guidelines

The Benefits of Regular Home Loan Pre-payments

Now that we have a basic understanding of home loans and prepayment let’s explore the numerous advantages of regularly pre-paying your home loan.

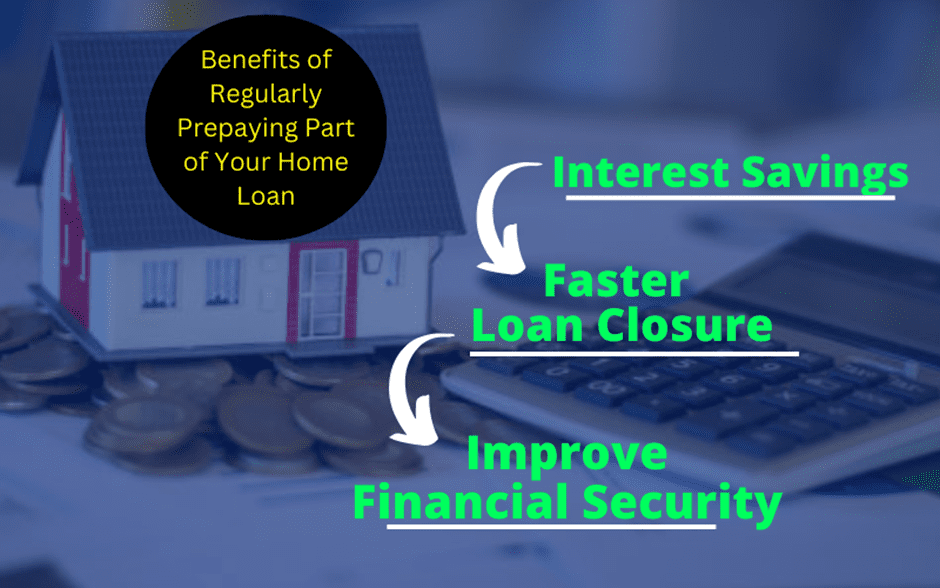

(1)Interest Savings

One of the most compelling reasons to make regular prepayments is the significant interest savings over the life of the loan. When you make additional payments towards the principal, you reduce the outstanding balance on which interest is calculated. As a result, you’ll pay less interest over the long term, potentially saving lakhs.

(2) Faster Loan Closure

Regular prepayments accelerate the process of paying off your home loan. Reducing the principal balance can shorten the loan term, allowing you to become debt-free sooner than planned. This can free up your cash flow for other goal investments such as retirement planning or your children’s education.

(3) Improve Financial Security

Paying off your home loan faster reduces your debt and enhances your financial security. Owning your home outright means you won’t have to worry about loan payments, providing peace of mind and financial stability during your lifespan.

Strategies for Regular Prepayments of Home Loan

Now that we’ve understood the benefits of regular loan prepayments, let’s explore some practical and effective strategies to incorporate this practice into your financial plan.

(A) Lump Sum Payments

Consider lump sum payment towards your home loan principal whenever you have extra funds, such as a bonus tax refund; this can immediately impact your loan balance.

Let’s compare the scenarios.

Scenario-1

Scenario-1 (Continue Loan As Scheduled)

Loan

1,00,00,000

Annual Interest Rate

8%

Loan Period in Year

20

EMI

83,644

Total Interest

1,00,74,562

Scenario-2

Scenario-2 (Extra Payment Made Annually- Rs. 5 lakhs)

Loan

1,00,00,000

Annual Interest Rate

8%

Loan Period in Year

20

EMI

83,644

Extra Payment Made Annually

5,00,000

Loan Period in Year Reduced To

9.6

Total Early Payment

47,50,000

Total Interest

43,20,065

Interest saved with Prepayment

57,54,497

The benefits of regularly pre-paying your home loan can clearly be seen in the above example. It doesn’t matter if it is a small or more significant amount. Prepayment is going to be helpful.

(B) Opt for a Higher EMI to Close Your Home Loan Faster

Choosing a higher Equated Monthly Instalment (EMI) is a strategic way to reduce both the interest outgo and the loan tenure. This method is particularly effective when your income increases—either through a salary hike or a job change.

When to Consider Opting for a Higher EMI

After a salary increment or promotion

When your monthly budget allows for flexibility

If you aim to become debt-free sooner and save on interest payments

Case Study: Sunil’s Home Loan Strategy

Let’s compare two options: (1) Investing surplus funds in a mutual fund SIP vs. (2) Increasing EMI and pre-paying the loan

Loan Details

Loan Amount: ₹42 lakhs

Interest Rate: 9.1%

Tenure: 20 years

Base EMI: ₹38,000

Surplus Available: ₹12,000/month

📈 Case 1: Investing ₹12,000 in Mutual Fund SIP (10% return)

Particulars

Amount

SIP Tenure

12 years

Total Principal Invested

₹17,28,000

Estimated Investment Value

₹33,17,000

Post-tax Amount for Loan Closure

₹31,68,000

Loan Outstanding after 12 Years

₹26,07,000

Excess Funds After Loan Closure

₹5,61,329

Home Loan Tax Benefit

₹7,20,493

Total Interest Paid (Post-Tax Benefit)

₹31,48,681

Result: Loan closed in ~12 years with an extra ₹5.61 lakhs in hand.

💸 Case 2: Increasing EMI to ₹50,000/month

Particulars

Amount

Loan Closure Time

12 years

Total Interest Paid

₹24,61,725

Tax Benefit on Interest

₹5,39,484

Total Interest (Post-Tax Benefit)

₹19,22,241

Result: Loan closed in 12 years with ₹12.26 lakhs less in post-tax interest outgo compared to Case 1.

What’s the Verdict?

While Case 1 provides surplus liquidity, Case 2 saves significantly more in interest—₹12.26 lakhs. Ultimately, choosing between investing surplus or increasing EMI depends on your financial goals and risk tolerance.

Key Factors That Influence the Outcome

Remaining loan tenure

Surplus amount available for EMI or investment

Home loan interest rate

Expected returns on mutual funds or other investments

Loan ownership (individual or joint)

Factors to Consider While Pre-Paying Your Home Loan

While pre-paying your home loan offers numerous benefits, it’s essential to evaluate several key factors before committing to this strategy.

1. Prepayment Penalties

Some banks or lenders impose penalties for early repayment of home loans, especially during the initial years of the tenure. Tip: Review your loan agreement carefully to understand if any prepayment charges apply and how they might impact your savings.

2. Maintain an Emergency Fund

Before you divert surplus funds toward prepayment, ensure that you have a sufficient emergency corpus. Why it matters: Having a financial cushion protects you against unexpected expenses, such as medical emergencies or job loss.

3. Evaluate Your Short-Term Financial Goals

Do you have upcoming short-term financial needs (e.g., education fees, travel, or home renovations)? Action: Prioritize saving for these goals first to prevent future cash flow issues.

4. Consider the Investment Opportunity Cost

Instead of pre-paying your loan, could your extra funds yield better returns elsewhere? Analysis: Compare your loan interest rate with potential returns from investments like mutual funds, FDs, or stocks. Prepayment might not always be the most profitable option.

Conclusion

Regularly pre-paying your home loan can bring significant benefits, including reduced interest costs, faster debt freedom, and greater financial peace of mind. By carefully assessing your financial priorities and using smart prepayment strategies, you can make the most of your surplus funds and secure a more stable financial future.

Pro tip: These strategies can also apply to other debts like car loans or education loans.

Robert J. Rousseau

Robert J. Rousseau has over 12 years of experience in the finance industry, specializing in investment strategies and portfolio management. He holds a degree in Finance from Stanford University and an MBA from Harvard Business School. Robert has worked in both the corporate and startup worlds, advising clients on managing and growing their investment portfolios. His writing combines technical expertise with a practical approach to investment, making complex concepts accessible to a broad audience. Robert is particularly passionate about emerging markets and sustainable investing.